When running a business, you learn to prepare for the unexpected. Retail insurance is an essential way for savvy retailers to make sure they’re ready for whatever life or business might throw at them. As a retailer, your most important job is growing your business, but it’s equally important to manage risk. You need to be able to identify potential pitfalls and take steps to protect your business.

This is why at Faire we set out to conduct a comprehensive survey of retailers today and find out how they use retail insurance. In this survey, we asked them questions about what types of insurance they choose, how they pay for it, and what they wished they knew before starting their search. As you’ll see, some of the findings might surprise you. Let’s dive into the data.

Why does insurance matter for small retail businesses?

As a small business owner, you’ve got a lot of balls in the air, but insurance is something to prioritize.

However, retail like any other venture, comes with risk, and retail insurance is a specific type of coverage designed to protect retailers against that risk. Imagine retail insurance as a safety net, covering everything from damage to your physical store to liability claims from customers who get injured on your property. This kind of insurance can also protect against other common threats, like employee theft, equipment failure, and business interruptions caused by natural disasters.

Getting the right insurance coverage helps ensure that one unfortunate event doesn’t mean serious financial issues. Whether you own a trendy boutique or a specialty grocery, retail insurance can be tailored to address the needs of your business. Ultimately, it safeguards the hard work and investment you’ve put into your business. This peace of mind means you can focus on making your business thrive and worry less about potential problems.

What key insights should you know about retail insurance?

Navigating retail insurance can get complex, so let’s break things down. Our survey reveals the latest about what kind of insurance small retailers are choosing, how they’re bundling their policies, and tips for selecting the right insurance provider. Check out the choices your fellow retailers are making and draw informed decisions about what works for you.

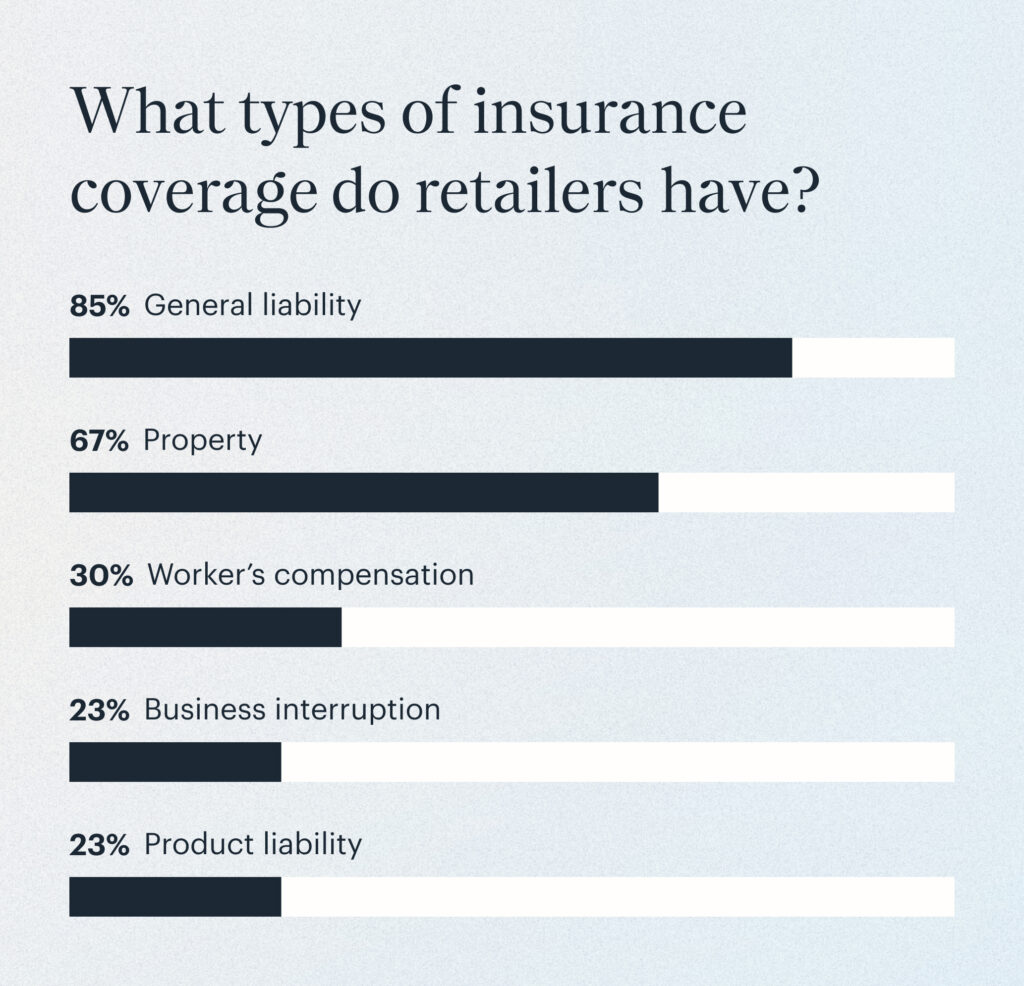

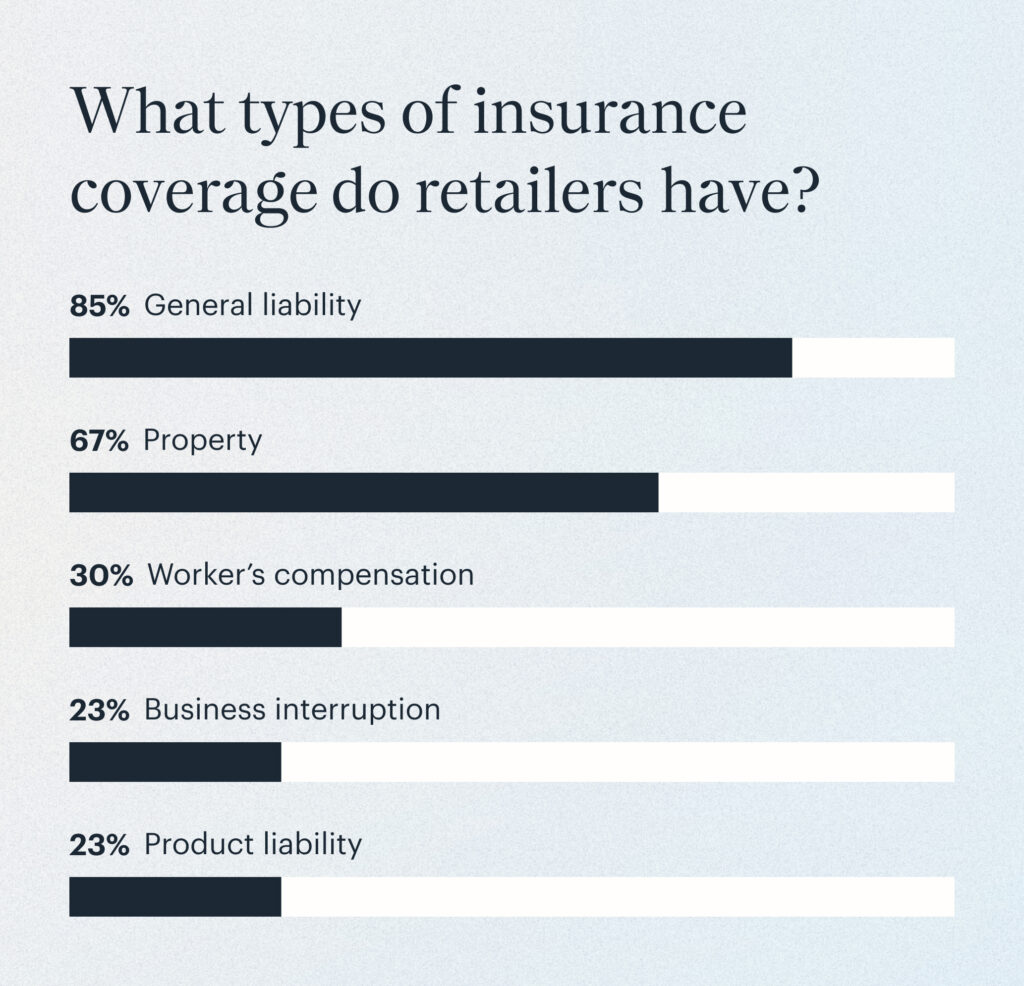

Popular insurance types

Though retail business owners are a broad and diverse group, most can agree on which insurance types are necessary. Most notably, 85% of small retailers opt for general liability insurance. General liability is essential for covering incidents involving customers and third parties. Not sure what these types of incidents are? Imagine a shopper slips on a wet floor in your store and gets hurt. This insurance makes sure you don’t foot the bill for their hospital visit. Given how many people can pass through a retail shop, the popularity of general liability makes sense.

Similarly, property insurance is chosen by 70% of the retailers and for the same reasons—retailers want to protect physical assets from damage or loss. Less common ones included business interruption and workers’ compensations, which 40% of respondents had, and product and cyber liability, which 30% and 25% had, respectively. However, the latter is becoming more important with the rise of e-commerce.

Policy bundling trends

Many retailers are small businesses and aren’t looking to break the bank for their retail insurance policy. This has led to a shift toward policy bundling, where insurers incentivize you to book multiple policies with them in order to save. (You might already have experienced this through your personal home and car insurance packages.)

About 60% of retailers surveyed picked fully bundled insurance packages for their businesses. This method makes multiple policies easier to manage and often results in some savings. However, about 25% prefer partially bundled policies, and 15% keep their policies separate, preferring customized policies that fit their specific needs.

Preferred payment cadences

How much they spend on insurance is important to retailers, but so is how they pay. When signing to a policy, you’ll have the option of paying annually, quarterly, or monthly. There are pros and cons to each end of the spectrum. Paying in lump sums can mean discounts on your premiums, but paying more frequently means you free up cash flow throughout the year and don’t get surprised by large bills.

When it comes to popularity, the majority of small retailers (55%) choose monthly payments for insurance premiums that are manageable. Meanwhile, 30% opt for annual payments, attracted by the convenience and potential discounts. A minority of 15% settle on quarterly payments, striking a balance between frequency and convenience.

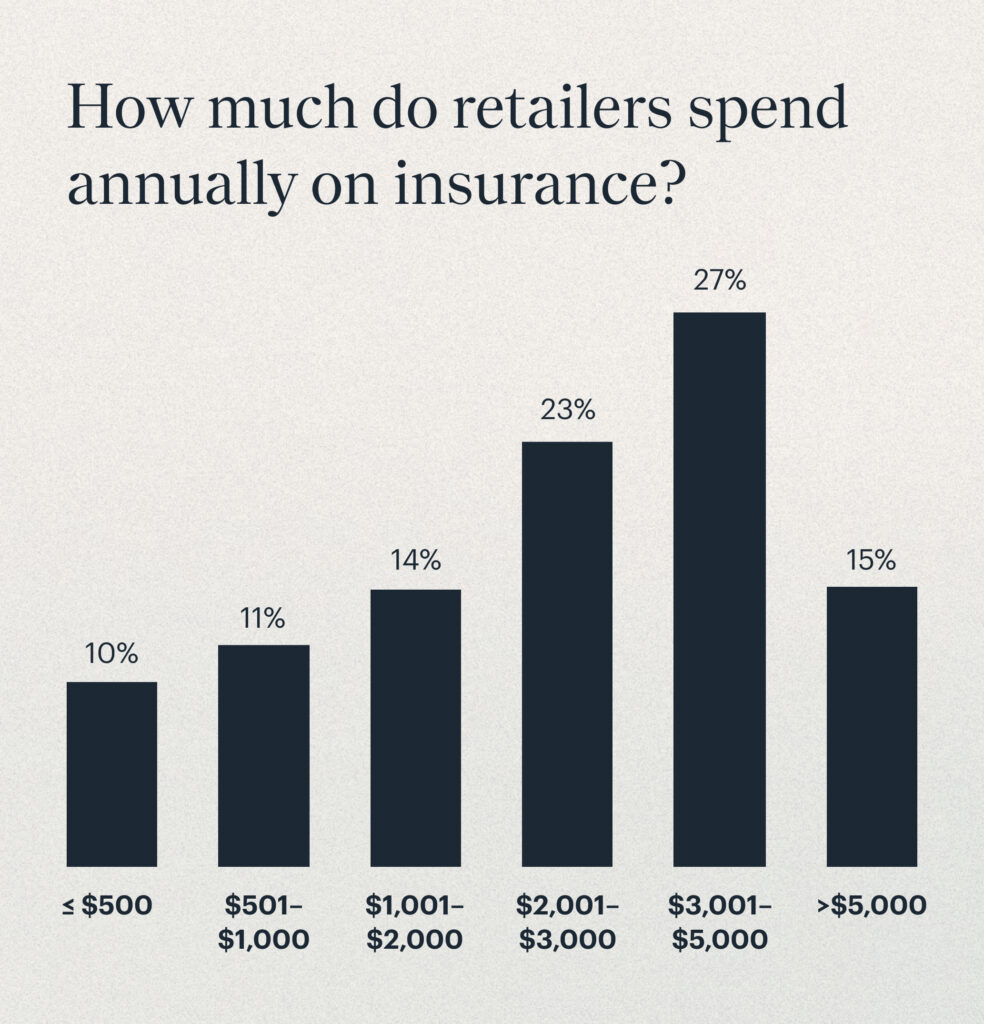

Spending habits

So when everything is said and done, and the insurance policy is inked, how much are retailers spending on their policies? This number can vary wildly because retailers have a wide range of needs and an even wider range of risk tolerance.

Ultimately, this is how it broke down: The data revealed that roughly 50% of small retailers spend between $501 and $2,500 annually on insurance premiums, or $81 to $250 monthly. This likely covers basic needs such as general liability and property insurance, suitable for many small retail spaces without specialized requirements. However, a notable group (10%) spends over $5,000 annually on insurance, indicating businesses that either operate in higher-risk environments, have more significant assets, or perhaps both. These retailers might opt for more comprehensive coverage or additional policies like cyber liability and product liability insurance to protect against a bigger scope of risks.

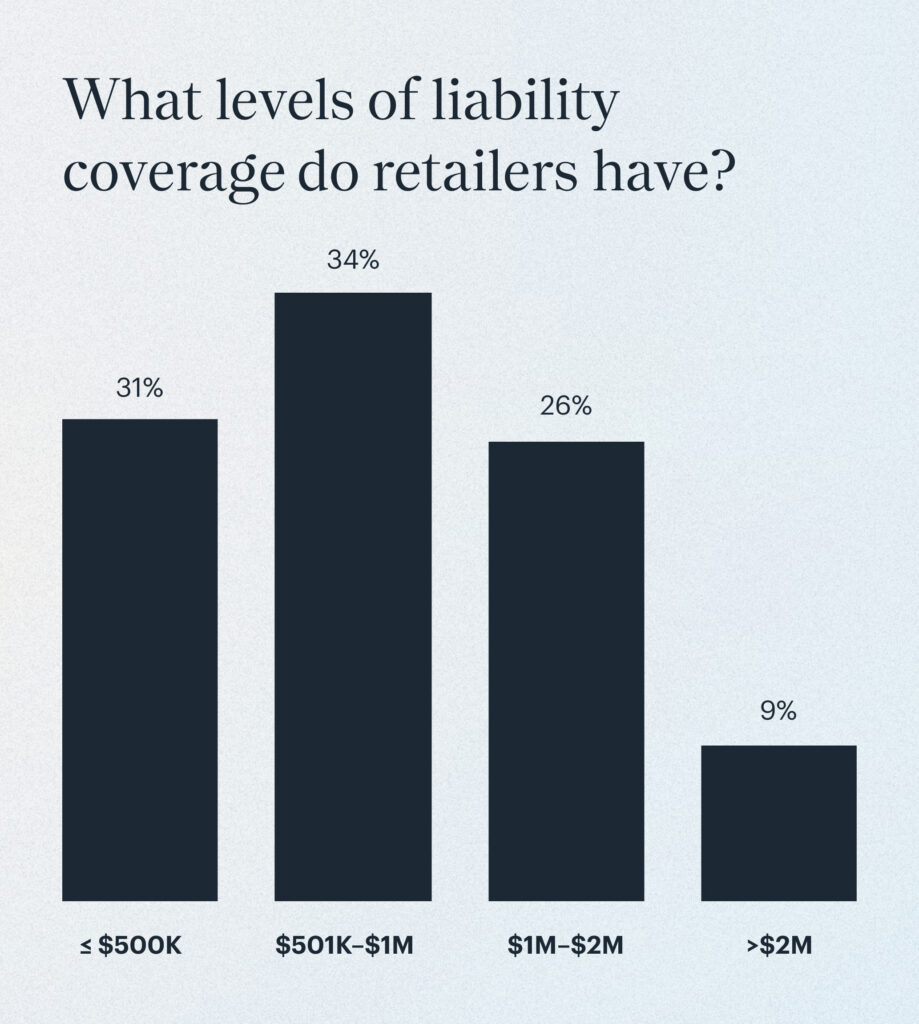

Insurance coverage levels

Similar to the question of how much to spend, how much coverage to get depends on your budget and risk tolerance. The range of coverage levels among these businesses usually falls between $500,000 and $1 million for general liability and up to $1 million for property insurance. Retailers have to walk the line between adequately protecting their assets and keeping insurance costs low. How much cover retailers decide to get can be influenced by the size of their business, their geographical location, and the value of their assets.

Top insurance providers

Once you know what you want in a policy, the hunt begins for the right insurance provider. A lot of small retailers lean toward established, household names like State Farm, Liberty Mutual, and GEICO. These companies aren’t just popular for their strong reputations—they also offer a wide range of options that cater to the diverse needs of different retail businesses.

A handy tip that respondents agreed on: Actively engage with insurance agents, and don’t shy away from getting multiple quotes. This approach really helps business owners get a better grip on what the market has to offer and find an insurance plan that not only fits the unique aspects of their business but also covers all their bases in terms of risks and liabilities. Essentially, it’s about making sure you’re getting the right protection.

What advice do retail business owners have to share?

Before you get overwhelmed by what to do and how to do it, our survey also gathered advice from 285 small retailers. We asked for their best tips about choosing retail insurance.

As we mentioned before, it’s wise to shop around. About 45% of those surveyed really recommend working with insurance agents to tailor coverage to fit your specific needs. Also, about 35% suggest getting multiple quotes. Many believe it pays to compare what’s out there, so you can land the best deal for your business. Lastly, don’t forget the importance of policy reviews—30% advocate for checking your policies annually. It’s all about making sure your insurance keeps up with the changes in your business and continues to meet your needs.

Not one size fits all

The major takeaway from our survey? It’s clear that small businesses are all about finding insurance that’s both simple to manage and easy on the budget. But they take different paths to unlocking that—whether it’s through bundled coverage, policy breadth, or policy provider. If you’re standing at the crossroads of choosing or rethinking your policies, learn from the insights of other small businesses. Taking some wisdom from your peers can help you find a policy that fits your particular needs and is just right for your business.

We want to help your budget go further. Apply for Open with Faire and get up to $20k in payment terms so you can stock your shelves worry free.